What is the impact of high inflation on pension schemes?

Pensions & benefits

This blog series reflects on recent global economic trends, and what these could mean for defined benefit pension schemes.

In this blog, Jasmine Bliss and Jonathan Wolff consider the impact and drivers behind the most significant inflation increases seen in recent years, and how trustees and sponsors can work together to manage what this means for their scheme’s journey.

Inflationary pressures have been mounting through 2022 and rising at pace across the world over recent months. This trend has been triggered by the start of an economic recovery from the pandemic interacting with a perfect storm of global events, including worldwide supply chain constraints and disruption, energy demand challenges following the fallout of the Russian invasion of the Ukraine, and labour shortages.

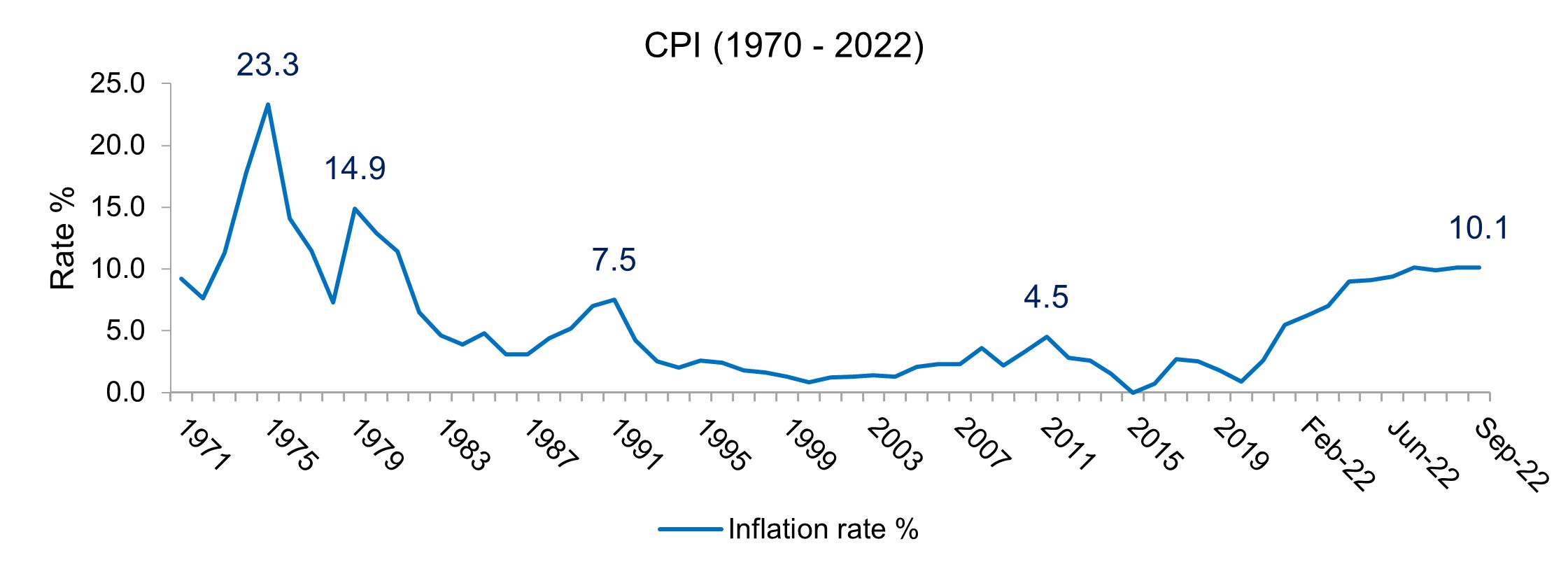

UK inflation is one of the highest amongst leading economies. The Bank of England currently forecasts that inflation could hit 13% in early 2023, with prices rising at a rate not seen since the 1970s.

How could inflation and the UK Government’s response to this impact your sponsor?

The rising prices create pressure on sponsors through several different channels. Firstly, increasing prices of raw materials, overheads, and wages can impact on profitability and cashflows. Rising energy prices can be very concerning for manufacturing industries as in-built protections such as price caps were previously not in place, as they are with consumers. Although the UK’s former Prime Minister, Liz Truss, announced short term energy price caps for businesses, charities and schools, and these have been affirmed by the new Prime Minister, Rishi Sunak, there is a real risk that energy and commodity prices will remain high over the longer term as macroeconomic headwinds persist.

Secondly, with central banks raising interest rates to combat inflation, businesses with a higher level of debt financing may also be more impacted than those which are not substantially leveraged. This is because falling margins, eroded cash reserves or reduced cashflows could cause lender concerns over adherence to banking covenants or could drive credit rating downgrades.

Increased interest rates can also impact refinancing, as obtaining new loans becomes more costly or the suite of lending options available to a sponsor could be reduced. We are already seeing companies finding it more difficult to raise finance as quantitative tightening measures are being pursued by central banks, and this trend looks set to continue. Looking ahead to the future, expansion plans or business strategies may need to change, for example postponing necessary investment to reposition the business to operate in a world rapidly turning its attention to the energy transition.

But inflation also isn’t always negative from a business perspective. Businesses which position themselves at the cheaper end of the scale may benefit from increased sales, as consumers with lower disposable income look for cheaper alternatives.

Ultimately, it is challenging to make generalised assumptions regarding inflationary impacts on businesses from a “top down” perspective. This is because each different organisation will experience the effects and make decisions based on its specific circumstances. This really highlights the importance of understanding the specific characteristics of the sponsor covenant, when assessing the impact of macroeconomic events.

An integrated approach remains key

Although sponsors may be experiencing inflation linked challenges, what about how inflation and rising yields are impacting upon pension schemes? The events of recent weeks have caused challenges to some schemes with liability driven investment strategies, and, now the dust has settled (hopefully!) we are encouraging all trustees and sponsors to review their strategic journey plan, to understand the impact of recent significant market shifts on their scheme’s funding position and investment strategy, and how they may need to refine their approach may as a result. Although a sponsor may be facing challenges, other factors may mean that a scheme is better or worse funded and hence has reduced or greater reliance on sponsor support so it’s important to consider the interaction here.

And what about from the perspective of members? For the past 30 years, many members of defined benefit pension schemes have been largely protected from inflation through in-built scheme mechanisms to increase or revalue benefits. But we are in a situation now where short term inflation is often above the caps on many pension increases, meaning for some there is a real reduction in the levels of benefits they are receiving. Some schemes are considering discretionary increases outside of the norm, potentially requesting additional financing requirements from a sponsor at a time that it itself may be challenged.

These dynamics highlight the importance of an integrated approach to considering a scheme and stakeholders. This is why, each year we release our Chart Your Own Course report. This helps our clients understand how complex events may impact the experience of their key stakeholders – be that member, sponsor or scheme. And, most importantly, it gives them the tools they need to design and manage effective strategic journey plans, ensuring that together, we are in the right position to managing an ever-changing world.